Managing your personal finances is crucial for achieving your financial goals and building a secure future. This guide provides a comprehensive overview of key aspects, from creating a budget to investing wisely and planning for emergencies. We’ll explore budgeting methods, saving and investment strategies, debt management techniques, and the importance of financial literacy. Get ready to take control of your financial destiny!

From understanding different types of savings accounts and investment options to navigating the complexities of debt and taxes, this guide will equip you with the knowledge and tools needed to build a strong financial foundation. We’ll cover everything from practical budgeting tips to long-term financial planning strategies, providing you with actionable steps to achieve your financial aspirations.

Budgeting & Tracking

Taking control of your personal finances is crucial for achieving your financial goals. A well-structured budget acts as a roadmap, guiding you towards financial stability and freedom. This section delves into the practical aspects of budgeting and tracking, equipping you with the knowledge and tools to manage your money effectively.A strong financial foundation is built on a detailed understanding of your income and expenses.

By meticulously tracking your spending and income, you can identify areas where you can save and invest wisely. This section Artikels various budgeting methods and tools to help you achieve this understanding.

Mastering your personal finances is a continuous journey, requiring meticulous planning and consistent effort. Understanding the intricacies of optimizing your finances is similar to mastering technical SEO, like learning the technical seo the complete guide , which requires deep dives into website architecture and code. Ultimately, both financial management and technical SEO demand a strategic approach to achieving optimal results.

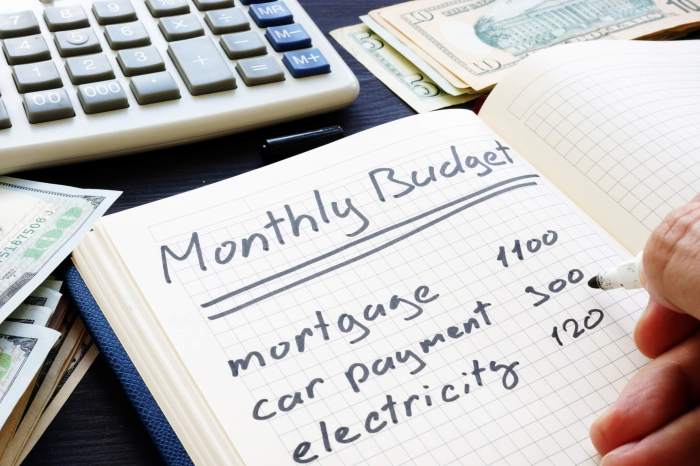

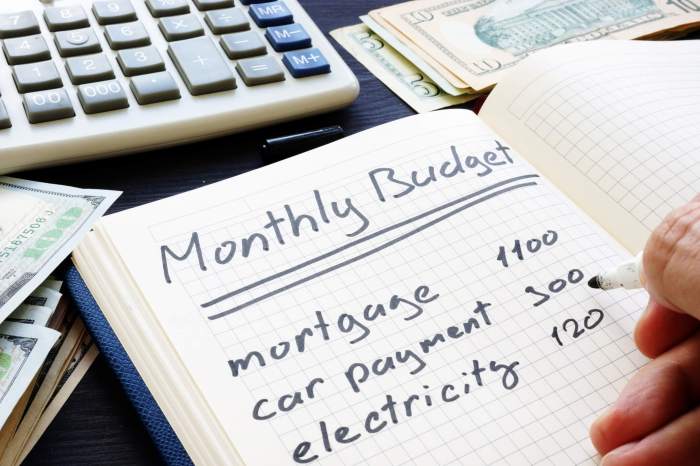

Creating a Personal Budget

A personal budget is a crucial financial tool that Artikels your income and expenses over a specific period. Creating a budget involves several key steps, ensuring that your spending aligns with your financial goals.

- Record Income and Expenses: Thoroughly document all sources of income, including salary, investments, and side hustles. Similarly, meticulously track all expenses, categorizing them into fixed, variable, and discretionary categories. This comprehensive record forms the foundation of your budget.

- Identify Financial Goals: Determine your short-term and long-term financial objectives, such as saving for a down payment, paying off debt, or investing for retirement. Defining these goals provides a clear direction for your budget.

- Categorize Expenses: Classify your expenses into fixed (rent, utilities), variable (groceries, entertainment), and discretionary (dining out, shopping). This categorization helps you understand where your money is going and identify areas for potential savings.

- Allocate Funds: Allocate your income to various categories, ensuring that your expenses and savings are appropriately covered. Prioritize essential expenses and allocate funds for discretionary spending based on your budget.

- Review and Adjust: Regularly review your budget to identify areas for improvement. Make necessary adjustments based on your spending patterns and financial goals. This iterative process allows you to adapt to changing circumstances and maintain financial stability.

Budgeting Methods

Different budgeting methods offer varying approaches to managing personal finances. Understanding the nuances of each method can help you choose the one that best suits your needs and lifestyle.

- Zero-Based Budgeting: This method allocates every dollar of your income to a specific category, ensuring that every dollar has a designated purpose. It provides a highly detailed view of your financial activities and encourages accountability. Pros: High level of control, pinpoints areas for saving. Cons: Can be time-consuming and overly detailed for some.

- Envelope Budgeting: This method involves assigning cash to different categories, representing the allocated amount for each expense. Pros: Encourages awareness of spending and limits impulse purchases. Cons: Can be inconvenient for online transactions.

- 50/30/20 Rule: This method suggests allocating 50% of income to needs, 30% to wants, and 20% to savings and debt repayment. Pros: Simple and straightforward; easy to understand and implement. Cons: May not be suitable for individuals with high debt or specific financial goals.

Sample Personal Budget Template

| Income | Expenses | Savings | Debt Repayment |

|---|---|---|---|

| Salary: $5,000 | Fixed: Rent ($1,500), Utilities ($200) | Emergency Fund: $500 | Credit Card: $300 |

| Variable: Groceries ($500), Transportation ($200) | Retirement Savings: $200 | ||

| Discretionary: Entertainment ($200), Dining out ($100) | |||

Tracking Tools and Apps, Managing your personal finances

Numerous tracking tools and apps offer different features and functionalities to monitor spending habits effectively.

- Mint: A popular budgeting app offering comprehensive expense tracking, analysis, and insights into spending patterns. Mint integrates with various financial accounts, streamlining the process.

- Personal Capital: This app goes beyond simple tracking, providing investment analysis and portfolio management. It helps users track their net worth and investment performance.

- YNAB (You Need a Budget): YNAB is a widely used budgeting app focused on zero-based budgeting, offering tools for detailed expense tracking and goal setting. It helps users allocate every dollar.

Comparison of Budgeting Apps

Different budgeting apps cater to varying needs and preferences. A comparison of their features and functionalities can aid in selecting the best fit for your financial goals.

- Mint vs. YNAB: Mint offers a more user-friendly interface for basic budgeting, while YNAB is designed for a detailed zero-based budgeting approach. YNAB emphasizes budgeting and tracking, whereas Mint emphasizes comprehensive financial analysis.

- Personal Capital vs. Mint: Personal Capital provides a more comprehensive financial overview, including investment tracking, while Mint focuses on expense tracking and budgeting.

Saving & Investing

Saving and investing are crucial components of a healthy financial plan. They allow you to build wealth, achieve financial goals, and safeguard against unforeseen circumstances. Understanding different saving and investment options, their risks, and appropriate strategies is essential for making informed decisions.Different types of savings accounts offer varying interest rates and features. High-yield savings accounts often provide higher interest rates compared to traditional savings accounts, encouraging more substantial savings.

Certificates of Deposit (CDs) typically offer fixed interest rates for a predetermined period, providing a known return but restricting access to funds during that time. Money market accounts provide higher interest rates than standard checking accounts and usually offer limited check-writing privileges.

Savings Account Types and Interest Rates

Various savings accounts cater to different needs and preferences. Traditional savings accounts offer basic savings options with modest interest rates. High-yield savings accounts provide a higher return compared to standard accounts, often attracting those looking to maximize their savings growth. Certificates of Deposit (CDs) offer fixed interest rates over a set period, providing a known return but restricting access to funds until maturity.

Money market accounts usually offer higher interest rates than standard checking accounts, typically providing limited check-writing privileges. Comparing interest rates from different institutions is crucial to find the best option for your needs.

Investment Options and Risks

Investing involves allocating funds to potentially grow wealth over time. Stocks represent ownership in a company, and their value fluctuates based on market conditions. Bonds represent a loan to a company or government, typically offering a fixed interest payment and potentially lower risk than stocks. Mutual funds pool money from multiple investors to invest in a diversified portfolio of assets.

Real estate investments involve purchasing property, offering potential appreciation but also significant upfront costs and management responsibilities. Cryptocurrencies are a relatively new investment asset class with high volatility and significant risk.

Investment Comparison Table

| Investment Type | Risk | Return Potential | Time Horizon |

|---|---|---|---|

| Stocks | High | High | Long-term (5+ years) |

| Bonds | Moderate | Moderate | Short-term to medium-term (1-10 years) |

| Mutual Funds | Moderate | Moderate | Long-term (5+ years) |

| Real Estate | Moderate to High | High | Long-term (5+ years) |

| Cryptocurrencies | Very High | Very High | Variable (Highly speculative) |

Building an Emergency Fund

An emergency fund is a crucial component of financial preparedness. It safeguards against unexpected expenses, like job loss, medical emergencies, or car repairs. A well-established emergency fund provides a safety net, reducing financial stress during challenging times. The ideal amount varies based on individual circumstances, but a 3-6 month cushion of living expenses is often recommended. Create a budget, track expenses, and prioritize saving to build this essential safety net.

Choosing a Suitable Investment Portfolio

Developing an investment portfolio involves carefully considering risk tolerance, financial goals, and time horizon. Conservative investors may favor bonds and stable mutual funds, seeking lower risk and steady returns. Moderate investors might balance stocks and bonds, seeking a moderate return with manageable risk. Aggressive investors may allocate more funds to stocks and other high-growth investments, potentially seeking higher returns but also accepting higher risk.

Diversification across different asset classes is essential for mitigating risk and enhancing potential returns.

Debt Management

Managing debt effectively is crucial for financial well-being. Uncontrolled debt can lead to significant financial stress and hinder your ability to achieve your long-term goals. A proactive approach to debt management involves understanding different types of debt, developing strategies for repayment, and actively working to improve your credit score.Debt, in its various forms, can significantly impact your financial future.

Careful planning and consistent effort are essential to achieving debt freedom and establishing a secure financial foundation.

Keeping your personal finances in order can feel overwhelming, but it’s totally manageable! One key aspect is boosting your online presence, and a great way to do this is by using a popup on your WordPress site to promote your Twitter page, like the method detailed in this helpful guide: how to promote your twitter page in wordpress with a popup.

This increased visibility can lead to more followers and engagement, ultimately helping you reach a wider audience and manage your personal brand more effectively. Ultimately, having a strong online presence can contribute to better money management strategies in the long run.

Types of Debt

Understanding the different types of debt you might have is the first step toward effective management. This knowledge allows you to tailor your repayment strategies to each type of debt. Different types of debt have varying interest rates and repayment terms.

- Credit Cards: Credit cards offer convenience but can lead to high-interest debt if not managed responsibly. High-interest credit card debt can quickly spiral out of control, impacting your credit score and making it difficult to achieve financial stability.

- Loans: Loans, including mortgages, auto loans, and personal loans, represent borrowed funds with fixed repayment schedules and interest rates. Understanding the loan terms is vital to avoid potential financial pitfalls.

- Student Loans: Student loans are often crucial for higher education but can create substantial debt burdens. Planning for repayment, possibly through income-driven repayment plans, is essential.

- Medical Bills: Unpaid medical bills can quickly become a source of significant debt. Establishing payment plans with medical providers or exploring debt consolidation options is often beneficial.

Debt Repayment Strategies

Developing a structured approach to debt repayment is crucial. Choosing the right method can significantly impact the time it takes to eliminate your debt. Two common strategies are the debt snowball and the debt avalanche methods.

- Debt Snowball Method: This method focuses on paying off the smallest debts first, regardless of interest rates. The psychological satisfaction of quickly eliminating smaller debts can motivate continued progress and build momentum.

- Debt Avalanche Method: This strategy prioritizes paying off debts with the highest interest rates first. By aggressively tackling high-interest debts, you minimize the overall interest paid over time. This method generally leads to faster debt elimination but might require a more disciplined approach, as the motivation is not the immediate gratification of paying off smaller debts.

Credit Scores and Their Importance

A credit score is a numerical representation of your creditworthiness, calculated based on your credit history. Lenders use credit scores to assess your risk as a borrower. Understanding and improving your credit score is essential for securing loans, renting an apartment, and obtaining credit cards with favorable terms.

A higher credit score indicates a lower risk to lenders, leading to better loan terms and lower interest rates. A low credit score, conversely, can lead to higher interest rates and increased difficulty in securing credit.

Strategies for Improving Your Credit Score

Maintaining a positive credit history is vital for a healthy credit score. Regularly monitoring and maintaining your credit report can be helpful. This includes regularly checking for errors and reporting any inaccuracies promptly.

- Pay Bills on Time: Consistent on-time payments are crucial for maintaining a strong credit score.

- Keep Credit Utilization Low: Keeping your credit utilization (the percentage of available credit you’re using) low is important. A low utilization ratio indicates responsible credit management.

- Avoid Opening Too Many New Accounts: Opening numerous new accounts frequently can negatively impact your credit score.

- Monitor Your Credit Report: Regularly checking your credit report helps identify any errors or inaccuracies that might be impacting your score.

Negotiating Debt Repayment Plans

Negotiating with creditors for more manageable repayment plans can be beneficial. In cases where you face financial hardship, contacting creditors directly to explore options for reducing interest rates or adjusting payment terms can be worthwhile.

Creditors are often willing to work with individuals facing temporary financial difficulties to create a more sustainable repayment plan. Communicating openly and honestly with creditors about your financial situation can lead to more favorable terms.

Financial Goals & Planning: Managing Your Personal Finances

Setting financial goals is crucial for achieving financial security and a fulfilling future. Without defined objectives, your money may be spent on immediate needs without consideration for long-term aspirations. A well-structured financial plan provides a roadmap for achieving your goals, ensuring you stay on track and avoid unnecessary financial stress.

Importance of Setting Financial Goals

Financial goals provide direction and motivation for your financial decisions. They act as benchmarks, helping you allocate resources effectively and stay focused on achieving desired outcomes. Clearly defined goals encourage responsible spending habits and promote a proactive approach to managing your finances. By setting specific, measurable, achievable, relevant, and time-bound (SMART) goals, you enhance your chances of success and build a strong financial foundation.

Different Types of Financial Goals

Financial goals can be categorized into various time horizons. Understanding these different types helps you prioritize your needs and allocate resources accordingly.

- Short-term goals are typically achievable within a year. Examples include saving for a vacation, paying off small debts, or building an emergency fund.

- Medium-term goals span from one to five years. These could include purchasing a car, upgrading your home, or increasing your savings for a down payment on a house.

- Long-term goals extend beyond five years and often involve major life events or significant financial objectives, such as retirement planning, funding your children’s education, or accumulating wealth for future generations.

Sample Financial Plan

A sample financial plan Artikels the steps needed to achieve your financial goals. The plan should be tailored to your individual circumstances, but the core principles remain the same. Start by identifying your financial goals, assessing your current financial situation, and developing a budget to track your income and expenses.

- Goal Setting: Identify short-term, medium-term, and long-term goals. Be specific about what you want to achieve and when.

- Financial Assessment: Analyze your income, expenses, assets, and debts. Understand your current financial standing.

- Budgeting: Create a detailed budget to track your spending and identify areas where you can save.

- Saving and Investing: Allocate funds for savings and investments aligned with your goals. Explore different investment options based on your risk tolerance and time horizon.

- Debt Management: Develop a strategy to pay off debts, prioritizing high-interest debts.

- Regular Review: Regularly evaluate your progress, adjust your plan as needed, and stay on track to achieve your goals.

Financial Goals and Timelines

A table illustrating different financial goals and their associated timelines.

| Goal | Description | Timeline | Estimated Cost |

|---|---|---|---|

| Emergency Fund | Savings for unexpected expenses | 1-3 months | $1,000 – $5,000 |

| New Car | Purchase a new car | 1-2 years | $15,000 – $30,000 |

| Home Down Payment | Save for a down payment on a house | 3-5 years | $20,000 – $100,000 |

| Retirement | Save for retirement | 20+ years | Variable, depending on lifestyle |

Significance of Financial Planning for Future Security

Financial planning is paramount for securing a stable and prosperous future. A well-defined plan ensures that your financial resources are utilized effectively, enabling you to meet your current needs while building a strong foundation for the future. It helps you achieve financial independence and avoid financial stress in the long run. This includes anticipating future needs, such as education costs or healthcare expenses, and creating strategies to address these challenges.

Financial Literacy & Education

Mastering your finances isn’t just about budgeting and saving; it’s about understanding the underlying principles. Financial literacy empowers you to make informed decisions, navigate complex situations, and build a secure financial future. It’s a continuous learning process, not a destination.Financial literacy is crucial for everyone, regardless of income level. A solid understanding of financial concepts allows you to avoid costly mistakes, maximize your earnings, and achieve your financial goals.

It helps you recognize and manage risks, making your financial life more predictable and less stressful.

The Importance of Financial Literacy

Financial literacy is the cornerstone of sound financial health. It equips individuals with the knowledge and skills to make informed decisions about money, fostering financial security and well-being. A strong foundation in financial literacy can lead to improved financial outcomes, reduced debt, and increased savings, ultimately contributing to a more fulfilling and secure life.

Resources for Improving Financial Knowledge

Numerous resources are available to enhance your financial understanding. Books, websites, and courses offer valuable insights and practical advice.

- Books: Numerous books offer comprehensive guides to personal finance. Authors like Dave Ramsey, Suze Orman, and Robert Kiyosaki provide practical advice and actionable strategies for managing your money effectively. Reading their books can offer insights into budgeting, saving, investing, and debt management.

- Websites: Reliable financial websites provide a wealth of information on various financial topics. Sites like Investopedia, NerdWallet, and the Federal Reserve offer articles, calculators, and tools to help you learn about investments, budgeting, and more.

- Courses: Online courses and workshops offer structured learning experiences. Many platforms provide interactive lessons, quizzes, and exercises to reinforce your understanding. These courses can cover specific areas like investing, retirement planning, or debt reduction.

Tips for Educating Yourself About Personal Finance

Cultivating financial literacy is an ongoing process. Consistent learning and application of knowledge are key to achieving financial success.

Mastering your personal finances is crucial, but often overlooked. Knowing how to allocate your resources effectively is key, and leveraging tools like those highlighted in the top 10 tools visible experts use to increase their personal brand can be a powerful boost. This list might seem unrelated at first, but the principles of strategic branding apply directly to personal financial management.

Ultimately, understanding your personal brand and how to effectively communicate your value can improve your financial decision-making.

- Start with the basics: Begin by understanding fundamental concepts like budgeting, saving, and investing. Build a solid foundation before tackling more complex topics.

- Seek out reliable resources: Use credible sources like reputable financial institutions, educational organizations, and qualified financial advisors to ensure accurate and up-to-date information.

- Practice consistently: Applying your knowledge through budgeting, saving, and investing is essential. Regular practice will solidify your understanding and help you develop good financial habits.

- Stay updated: Financial markets and regulations change over time. Continuously update your knowledge to stay current with the latest trends and best practices.

Key Financial Concepts

Understanding key financial concepts is essential for making informed decisions. These concepts form the bedrock of effective financial management.

| Concept | Explanation |

|---|---|

| Budgeting | A budget is a plan for how you will spend your money. It helps you track your income and expenses, ensuring you’re spending within your means. |

| Saving | Saving involves setting aside a portion of your income for future needs or goals. Regular saving builds a financial cushion for emergencies and allows you to achieve long-term goals. |

| Investing | Investing involves putting your money to work to earn a return. It’s a crucial component of wealth building, but involves risks. |

| Debt Management | Debt management involves strategies to control and reduce outstanding debts. Understanding different types of debt and creating a plan for repayment is key to financial health. |

Example of Financial Planning

A 25-year-old, earning $50,000 annually, may prioritize saving for a down payment on a house within five years and contributing to a retirement fund. Understanding their financial situation and establishing a plan are key steps toward achieving these goals.

Emergencies & Unexpected Expenses

Life throws curveballs, and having a plan to navigate unexpected expenses is crucial for financial well-being. Ignoring these potential disruptions can lead to significant stress and hinder your long-term financial goals. This section dives into the importance of proactive planning for emergencies and Artikels strategies for managing them effectively.Unexpected events, from medical emergencies to job loss, can quickly deplete savings and disrupt financial stability.

By understanding the importance of a financial safety net and developing a plan, you can navigate these challenges with greater confidence and resilience.

Importance of Planning for Unexpected Events

Unexpected events, whether personal or external, can drastically impact financial stability. Planning ahead mitigates the potential damage and allows for a more controlled response. A well-structured plan ensures you’re prepared for potential setbacks, minimizing the financial strain and allowing you to focus on recovery.

Steps to Take When Facing a Financial Emergency

Managing a financial emergency requires a systematic approach. The following steps provide a framework for handling these situations:

- Assess the situation thoroughly. Determine the nature and extent of the emergency, noting all associated costs.

- Review your budget and identify areas where you can cut back. This might involve reducing non-essential spending or negotiating with creditors for better terms.

- Explore available resources. Consider borrowing from family or friends, utilizing credit cards with favorable interest rates, or seeking assistance from community support organizations.

- Prioritize essential expenses. Ensure you’re meeting your fundamental needs first, like housing, food, and healthcare.

- Create a repayment plan. If you’ve incurred debt, develop a plan for paying it back, even if it means making smaller payments initially.

Need for Insurance (Health, Life, Home)

Insurance acts as a crucial safety net, protecting you from substantial financial losses due to unforeseen events. It’s vital to have adequate coverage for health, life, and home.

- Health insurance provides coverage for medical expenses, including hospital stays, surgeries, and doctor visits. This can prevent catastrophic medical bills from overwhelming your finances.

- Life insurance replaces lost income if a breadwinner passes away. It provides a financial cushion for dependents and helps cover outstanding debts.

- Home insurance protects your property from damage caused by natural disasters or accidents. This protects your investment and ensures you can rebuild if necessary.

Strategies for Managing Unforeseen Expenses

Building a financial safety net involves more than just insurance. Proactive strategies help you weather unexpected storms.

- Emergency fund: Establish a dedicated fund to cover unforeseen expenses, aiming for three to six months of living expenses. This fund acts as a financial buffer against unexpected events.

- Budgeting: Regularly review and adjust your budget to incorporate potential emergencies. This involves understanding where your money goes and identifying areas for potential savings.

- Flexible spending: Designate a portion of your budget for unexpected expenses. This allows you to address unforeseen situations without derailing your overall financial plan.

- Contingency planning: Develop a plan for various scenarios, such as job loss, medical emergencies, or home repairs. This helps in navigating unexpected situations with more ease.

Importance of Having a Financial Safety Net

A financial safety net is essential for peace of mind and stability. It protects you from significant financial setbacks, allowing you to focus on your well-being and future goals.

“A financial safety net provides a sense of security, enabling you to handle unexpected events with resilience.”

A strong safety net reduces stress and allows for more controlled decision-making during difficult times.

Tax Management

Understanding tax implications is crucial for effective personal finance management. Taxes are mandatory payments to governments at various levels, and a comprehensive understanding of how these payments impact your finances is essential. Knowing your tax obligations allows you to better plan your income, savings, and investments. This section will delve into the different types of taxes, the filing process, strategies for minimizing tax liabilities, and the importance of accurate record-keeping.Different taxes, including income tax, sales tax, property tax, and others, significantly impact your overall financial picture.

These taxes can vary based on location and income levels, making it essential to understand your specific obligations. This understanding is fundamental to managing your finances and planning for the future.

Understanding Tax Types

Various tax types affect your financial decisions. Income tax is levied on earnings from employment, investments, and other sources. Sales tax is added to the price of goods and services, while property tax is based on the value of your property. Understanding the different types and how they apply to your specific situation is critical to managing your finances effectively.

These taxes can vary based on location and income levels.

Filing Taxes

The tax filing process involves gathering documentation, calculating your tax liability, and submitting the required forms to the appropriate tax authority. This process can be complex, and seeking professional help from a tax advisor can be beneficial, particularly for those with intricate financial situations.

Strategies for Minimizing Tax Liabilities

Various strategies can help minimize tax liabilities. Tax-advantaged accounts like 401(k)s and IRAs can reduce your taxable income. Itemizing deductions instead of taking the standard deduction, if applicable, can potentially lower your tax burden. Strategic investments and contributions to tax-advantaged accounts can often provide substantial long-term savings.

Keeping Accurate Financial Records

Maintaining accurate financial records is paramount for tax purposes. Detailed records of income, expenses, and deductions are essential for accurately calculating your tax liability and for potential audits. These records should be meticulously maintained throughout the year to facilitate a smooth and efficient tax filing process. Accurate records allow for easy calculation of deductions, credits, and other tax benefits.

Example of Tax Implications

Imagine a single individual earning $50,000 annually. If the applicable tax rate is 20%, their tax liability would be $10,000. Maximizing deductions and utilizing tax-advantaged accounts can significantly reduce this liability. Consulting with a tax professional can help you explore options tailored to your specific financial situation.

Final Summary

In conclusion, mastering your personal finances is a journey, not a destination. By understanding budgeting, saving, investing, debt management, and financial planning, you empower yourself to build a secure financial future. Remember, financial literacy is key, and continuous learning and adaptation are essential for success. Take control of your finances today, and watch your financial well-being flourish!